When you’re young, you have time to take more risks. That’s something I say to clients who come into our offices interested in variable annuities and variable life insurance. Now, we don’t offer variable products as a wealth preservation firm and choose not to be licensed to offer such products, but more than a few of our clients are curious about these types of policies. Variable life insurance policies and annuities are investments and higher risk ones at that.

That’s why we usually recommend our clients buy fixed products, and if they’re looking for a higher return, fixed-index products. Indexed insurance products are not risky investments and tend to be a much safer way to build long-term, sustainable wealth for our safety minded clientele.

Often, alternative wealth building products are popular among older investors. They allow you to continue taking risks while finding a way to hedge your bets. These alternative wealth building strategies are diverse and come in varying levels of risk. They’re also managed by different entities and guaranteed in different ways. When choosing between the fixed and variable options in annuities and life insurance, what you choose will depend on your ultimate goal, whether that goal is building wealth for yourself or others.

Starting with the Basics: Building Wealth with Life Insurance And Annuities

Annuities and life insurance, while both good for wealth building, are entirely different products. In fact, you could say they have an inverse relationship to each other. Life insurance is designed to hedge the risk that you pass away younger than expected and don’t have anything to leave behind for heirs. Annuities, on the other hand, are insurance designed to protect you if you outlive your savings.

| Life Insurance and Annuities At a Glance | ||

| Life Insurance | Annuities | |

| Who benefits? | The heirs of the insured | The owner/annuitant |

| What does it provide? | A lump sum to a beneficiary | A series of ongoing payments |

| Who pays the most? | Older individuals in poor health pay higher premiums. | Younger individuals in good health have lower payouts. |

| What are the tax implications? | Most policies are purchased after tax and provide tax-free benefits. In addition, policies can be used as a tax shelter for estate taxes. | Policies can be purchased with pre-tax dollars as well and proceeds may be taxable as well. |

| What risk is it designed to limit? | Dying too soon | Prevents the possibility of outliving your savings |

Who Needs Life Insurance and How It Builds Wealth

For purposes of this page, when we talk about life insurance, we’re specifically talking about universal life policies that offer a tax-free death benefit and may have a cash value component as well. What happens is you get a quote for a premium. That premium is broken up into portions. A part of it is used to keep the death benefit in force, while the remainder is used to grow cash value. That cash value can later be borrowed against, cashed out, used to pay premiums, and rolled into new policies.

Life insurance policies are especially useful for anyone looking to provide for heirs while also helping those heirs avoid estate taxes. It can also be used to fund several charitable causes. Finally, in some cases, it can be used as a back-up pool of funding for retirement, again by leveraging the cash value and the potential tax free access to the cash that life insurance provides. Despite that, this is a less common use for life insurance because when most think of retirement saving with insurance, they think of annuities.

Who Needs Annuities and How They Stretch Out Income

Annuities are also insurance policies, but they’re designed to provide funding for the annuitant/owner, rather than their heirs. Annuities can be a safer bet for creating ongoing retirement income, and they can be used to supplement underfunded nest eggs. Annuities typically come in two forms:

- Immediate. An immediate annuity, sometimes called a single premium immediate annuity (SPIA), is bought with a lump sum upfront. Following the payment of the premium, the individual will receive regular payments for a set period or for the rest of their life, or a period certain depending on the terms of the contract.

- Deferred. A deferred annuity is one that needs time to vest. In this case, the annuity will go through an accrual period when it will earn interest. After the accrual period, the annuity will begin making payments, again based on a preset schedule.

There are many different forms of annuities and life insurance policies available, depending on your eventual goal. However, one big factor to consider is how these policies earn interest.

Variable vs. Fixed vs. Fixed Indexed: What’s the Difference?

The only thing fixed, fixed-index, and variable annuities and life insurance have in common is their name. Everything else, from how they’re handled to how they earn money and how they’ll eventually pay out, is completely different. Fixed is probably a bit simpler to understand.

How Fixed Contracts Guarantee an Interest Rate

When you buy a fixed annuity or life insurance policy, the company says to you, “Your return is X% and is an agreed-to percentage. Regardless of the economic climate, that percentage doesn’t go down because your money is never directly invested in the market. Fixed policies are market risk-free options for conservative financial planning.

However, some may be disappointed with their return because fixed policies typically offer the lowest interest rates. To gain a better return, some may seek out riskier options. On the other end of the spectrum, both in market risk and complexity, is the variable annuity or life insurance policy.

Why Variable Contracts Are for Risk Takers

Despite their name, variable life insurance and annuities are technically investments. In fact, they are legally defined as securities. Since we have chosen not to be licensed to offer securities, we can’t offer variable type programs. In these programs, the portion of your policy that makes up your cash value is directly invested. Thus, these instruments may see a better short-term gain, which is why they’re often recommended for younger individuals. If the market crashes, the value will go down. It’s possible to lose money on a variable policy. These types of policies are sold by investment firms and as already stated, require appropriate federal licenses to service.

With our client base, we generally don’t recommend variable annuities or policies because security is more important to them than earning a bigger return. For clients who do want to see a little bit of a gain from the market, we recommend a different type of fixed policy. That type is known as the fixed-index policy.

Fixed-Index Life Insurance and Annuities Offer Diversity

Fixed-index annuities and insurance policies are relatively new concepts, although they have been around since 1995. These policies offer a fixed-rate option, however, additional earnings can be made on the gain in a specific index. These policies have the potential to earn more and avoid the risk of loss present in variable annuities.

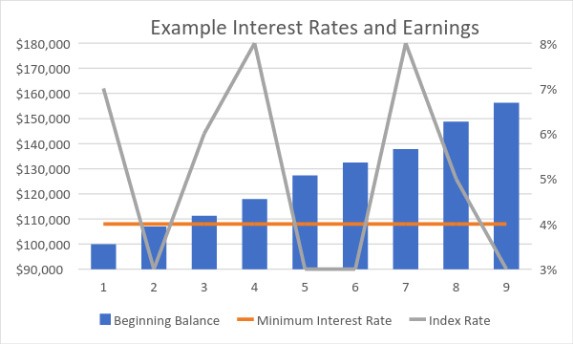

Here’s how it works. You get a fixed-index annuity with no cap and a 2% spread. Since it is uncapped, the sky’s the limit. However, if your index delivers 10% return in a given year, you would net 8% since the 2% spread goes to the insurance company. This is much more advantageous than a fee arrangement in which a 2% fee is charged even if you have losses, further deteriorating your principal.

With a spread, the client and the insurance company are on the same side of the table. When the client wins, the insurance company gets paid. In a flat or negative year, the client never loses and the insurance company does not earn the spread. If the client opts for special bonuses or riders, there can be a small charge in all years. It should be noted that some fixed index annuities charge no fee and no spread!

How this would impact your wallet would depend on whether you’re buying a fixed-index annuity or a life insurance policy. With an annuity, this would create an opportunity to earn greater payments when the payments begin and provide higher account balances and death benefits. Some annuities offer a special “income rider” that guarantees a preset rate of growth on the “income value,” which ultimately determines how much income you will receive.

The income value is not the accessible cash value, but rather, an amount of money based on your initial investment that is compounded at a predetermined rate over time for income calculation purposes. The higher the income value is over time, the higher the potential guaranteed income.

For example, an annuity may offer a 7% compounded interest rate on the income value “roll up,” even though the account value may earn much less based on the index performance. For income purposes, the 7% will determine the ultimate value used unless the index outperforms the 7% over time. This adds a measure of predictability to the client’s income scenario because we can tell them, based on future age and the roll-up percentage, exactly what the income for life guarantee will be at any point in the future, which is very important.

With an indexed life insurance policy, the cash value gets earnings based on the market index. The policy death benefit will pay out a specific amount because part of your money is paying for the premium. However, a portion of that money goes into cash value, which can be borrowed or rolled back into the policy. This cash value will see gains based on market fluctuations, making the policy more valuable when you do need to use it.

Fixed-index policies allow you to create enhanced results without the risk of variable contracts, which is why we generally recommend these for our clients. However, there are a few overall concerns you need to consider for all indexed annuity and insurance products. While they are market risk free, there are a few things to be aware of.

When an Insurance Contract Underperforms

There are a few things you need to look out for when buying indexed products. First, these policies typically have surrender periods. If you cash one out before the surrender period is over, you could wind up paying hefty fees.

In addition, you need to consider the tax implications. Often, annuities are purchased with pre-tax funds, which makes them qualified annuities. So, if you purchased a deferred annuity under one of these programs and now decide you want to get rid of it, you’ll have to pay tax on it when you cash it out.

There are several reasons you may want to get rid of a life insurance or annuity contract. Here are a few to consider:

- A return that doesn’t keep up with inflation or performs poorer than expected.

- High maintenance fees that cut into the overall policy profit.

- High premium costs that make the policy unaffordable.

- Changes in a life circumstance that make the policy unnecessary.

After reading through all the various contracts you own, you may be concerned that you’ve purchased the wrong ones. First, if you’re dealing with an annuity that was purchased with pre-tax dollars, a qualified transfer may be the best option for you.

How a Qualified Transfer Works

When you buy an annuity with pre-tax dollars, you have to pay the taxes eventually. The goal is that you’ll pay taxes at a lower rate when you’re living off the income in retirement, but other events can trigger taxes as well. One of the most common is a policy cash out in which you surrender the policy for a gain.

When you do this, you’re going to have to pay taxes. However, the IRS recognizes that needs change and policies grow outdated. As such, they allow individuals to exchange an outdated policy for a newer one.

A qualified transfer can be a good option if you’re concerned regarding the tax implications of your policy. These transfers allow you to move money into other qualified accounts without accelerating taxes, as long as you transfer the annuity assets without changing the tax qualified character of the assets.

However, if you’ve purchased an annuity with after-tax dollars, a 1035 Exchange may be the solution to avoid unnecessary taxes.

- The policy must be traded for the same type (an annuity for an annuity, life insurance for life insurance).

- The insured must be the same.

- Several policies can be traded for one, but the overall value must remain the same to qualify for a tax-free exchange.

- Loans should be paid off prior to the exchange because the loan will be considered a disbursement if outstanding.

Selling a Policy to a Third Party

Both life insurance and annuities can be sold to third parties, provided you have the right type of policy and other conditions are met. With an annuity, generally, you’re selling the right to future payments on the annuity for a lump sum upfront. On life insurance, you can sell the policy to a third party for less than the death benefit but more than the cash value. In some cases, you can even retain some of that death benefit. You generally need to be old or in poor health with a relatively short life expectancy for the policy to be attractive to an institutional investor.

Taxes for these sales are going to depend on if the product was bought with after-tax money, what the cost basis of the policy is, and other factors based on your own circumstances. Also, not all insurance policies will be appealing to buyers, which is why it’s important to review any sales decision with a financial professional.

At Howard Kaye, we provide a full policy review for our clients and offer a range of alternative financial options for wealth building. We can help create strategies to stretch out your savings, protect your assets, and minimize your tax bill. For more information, contact us at 800-DIE-RICH.