Portfolio Insurance

An Asset Protection Strategy for Wealth Creation and Preservation Late in Life

If you’re like most of our clients, you know that building wealth late in life can be a challenge. You’ve probably also heard the advice to reduce your portfolio risk as you age, which makes wealth creation even more difficult.

Well, we had an older client who had an aggressive stock portfolio — and he was extremely proud of it. His wife, on the other hand, wanted him to get rid of it. She thought that, at his age, he was too old to have such a high-risk investment strategy.

So we came up with a way to make them both happy — our portfolio insurance plan. This allowed the husband to keep his stocks and continue investing. Meanwhile, his wife gained the security of knowing the money was protected.

Portfolio insurance is an asset protection strategy we offer using life insurance. It can allow you to continue to invest and create wealth into your later years while keeping your money secure to pass on to heirs.

How Portfolio Insurance Works

At Howard Kaye, we think it’s silly to make our clients completely reduce risk as you age. After all, most of our clients are experienced wealth builders. You get better at making investment decisions as you age because you have the benefit of years of market knowledge. Rather than wasting that experience, we think you should continue using your smart investing strategies. You just need to insure that investment.

Big companies do this same thing. Many financial firms use insurance as a safety net so they can stay solvent even during a market crisis.

Our portfolio insurance strategy does the same thing for our clients, just on a smaller scale. We look at the overall value of your portfolio, your breakeven point, and any possible tax deductions. Then, we help you buy an insurance policy equal to that amount.

Consider this example:

A client comes to us with a portfolio valued at $5 million. The client tells us she initially purchased the portfolio for $3 million and has seen $2 million in gains since then. The client’s breakeven point is $3 million, but she also wants to protect the gains.

In this instance, we would look at the floor. If the stock has a $1 million floor, we’d recommend she insures based on the $4 million maximum she could lose. If there is no floor, which is common in higher-risk investments, we would recommend insuring slightly less than $5 million. Some clients, instead will choose to insure a percentage of their investment portfolio. For example, a client with a $5million investment portfolio might insure the portfolio for $2.5 million using a 50% ratio.

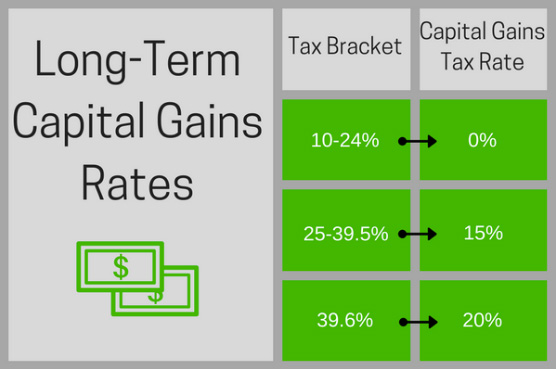

And, you need to remember that the insurance has a benefit the stock payout doesn’t — it’s tax free. Sometimes, we will reduce the overall capital gains tax amount from the value of the portfolio. In the above example, if the entire portfolio was sold, there would be about a 15% reduction for capital gains tax, based on the tax bracket the client is in (the tax bracket is based on factors such as income and filing status). The client might choose to insure the value of the portfolio for $4.25 million based on $750,000 being collected in taxes. The table below shows the capital gains tax rates based on your tax bracket.

Our clients are essentially able to discount the insurance they need to buy because of the reduction from taxes. If the portfolio continues to do well, the portfolio insurance can even be repurposed as a source of funding to cover the eventual capital gains tax.

Our clients are essentially able to discount the insurance they need to buy because of the reduction from taxes. If the portfolio continues to do well, the portfolio insurance can even be repurposed as a source of funding to cover the eventual capital gains tax.

What Happens When the Value Changes?

When discussing our portfolio insurance strategy, the first thing many clients ask is: “What happens when the stock market changes?”

If the stock drops suddenly, the death benefit of the policy will back it up, so your heirs won’t have to realize the loss. On the flip side, if the stock doubles in value, your insurance will provide a greatly enhanced legacy to your family and favorite charities. Another option is you could reallocate a portion of the gains to a guaranteed program, like a fixed-indexed annuity, where there is upside potential to see market gains but no market loss.

Our portfolio solutions help our clients sleep easier at night while still enjoying the benefit of their smart investments. Rather than completely reducing risk and diminishing investment performance as you age, you can take risks and back them up with insurance. This process allows our clients to continue building wealth late into their lives while leaving behind a legacy for heirs. For more information on our portfolio insurance strategy, contact a Howard Kaye advisor today at 800-DIE-RICH.

Source: “Topic 409 – Capital Gains and Losses.” Irs.gov. The Internal Revenue Service. 2016. https://www.irs.gov/taxtopics/tc409.html

Non-Qualified Annuity Beneficiary Distribution Tax Options: How to Protect Your Investment—and Loved Ones

Non-qualified annuities—that is, annuities that are not part of an IRA or other tax-qualified retirement plan—can serve as a valuable component of your financial and estate plan. However, Non-qualified annuities […]

Tax-Sheltered Annuity Benefits: What Investors Must Know (and Advisors Won’t Tell You)

Clients often approach us seeking advice on how to choose from the dozens of financial products that are available for retirement. The second half of this question is often, “…and […]

When You Need a Trust to Protect Elderly Relatives and Transfer Wealth

People who take advantage of the elderly are more common than you may think. Which is why it isn't uncommon for us to discuss with clients using a trust to [...]