Life Settlements

An Asset Protection Strategy for Wealth Creation and Preservation Late in Life

Sell Your Unwanted Life Insurance Policy

“I think I’m just going to cash surrender it.” We hear those words more often than we would like to when it comes to permanent life insurance. When a policy becomes unaffordable or unnecessary, most think the best idea is to surrender it, while others let it lapse for nonpayment. We want to show you how you could get up to 4x more with a life settlement vs cash surrender value.

We recently had been referred to a client who was going to surrender a large life policy that had a $72,000 cash surrender value. After visiting with Howard Kaye, he listed the policy for sale on the secondary market and received $2.7 million in cash a few months later!

Do not assume that cash surrender is your best option. That can be a huge mistake. In our experience, simply surrendering a policy without considering a life settlement can result in leaving money on the table. Instead, the best choice is to explore life settlements, which provide cash up front and, in some cases, offer paid up death benefits, or a combination of both.

Why People Give Up Policies

There are two reasons people give up policies: They either find them too expensive or believe they’re unnecessary.

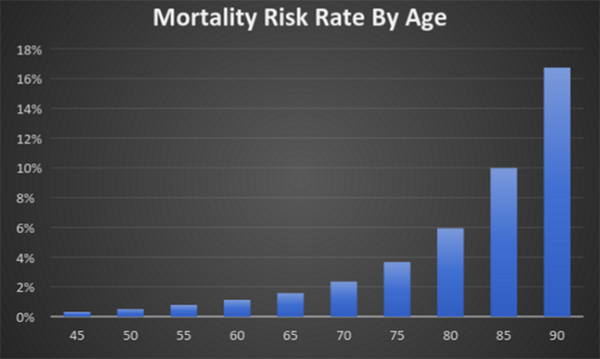

As we age, a larger portion of premium payments goes to keeping the death benefit in force. That’s because our risk increases as we get older and the policy charges are changed to reflect that.

Based on current data for nonsmoking males in the United States from the U.S. Social Security Administration

Based on current data for nonsmoking males in the United States from the U.S. Social Security Administration

The second reason is simpler: The policyholder just doesn’t need the policy. Several states have passed laws amending or even eliminating their estate tax. Also, there have been changes to the federal estate tax rate that may have reduced the overall burden.

In 2001, for example, the top tax rate was 55%. Fifteen years later, that rate was reduced to 40% and the exemption for couples is about $11.7 million. Someone who bought a policy back then may now find that estate tax isn’t as much of a concern. That’s when they might consider surrender of their policy.

That’s simply throwing money down the drain. When you have a permanent policy, you have a valuable asset. Even some term policies can be converted and sold in the life settlement marketplace.

How the Life Settlement Process Works

When you have a whole life or universal life insurance policy that you want to get rid of, you may be able to sell it for much more than the cash value and even retain some of the death benefit. This process is known as a life insurance settlement. Mainly, you’re selling the right to the future value of the policy in exchange for a payment now. The process involves three basics steps:

- Appraisal. During the appraisal, the company or broker will review your existing policy and tell you if it’s eligible for sale and what you can expect to receive for it. The total offer will be dependent on the death benefit, the cash value, and your own mortality rate. In most cases, life insurance buyers prefer to purchase policies with a low cash value and a high mortality rate, from individuals over the age of 65. This is how they’ll see the largest return as they’re buying the policy for the death benefit.

- Bidding. The thing to remember is that the appraised value isn’t fixed. You can get a ballpark figure and then shop around to see what those in the market are willing to pay. This competition increases the value, so you get the highest payout or the highest retained death benefit.

- Settlement. Once you find a bid you like, then you move onto the settlement process. This involves completing all of the necessary paperwork, changing policy owners, and signing the life settlement contract. At that point, the seller receives their payment and the buyer takes over the old policy.

These steps will remain virtually the same whether you’re looking for a high cash offer, a high retained death benefit, or a combination of both. The key here is that you need to work with the right person who has access to the secondary markets you need. The more bids you get on a policy, the more you get out of it.

At Howard Kaye, we offer a policy review and a life settlement option for those who want out of an old policy. We use our connections to drive competition for your policy, allowing you to maximize your payout, death benefit retention, or in some cases, both. Rather than giving up that life insurance policy, contact a Howard Kaye advisor at 800-DIE-RICH to discuss our services in the life settlement market.