Retirement planning funds have become increasingly accessible, with most employers now offering top-tier 401(k) plans that include multiple investment options and contribution matching. Alternatively, anyone with a few thousand dollars to invest can walk into any branch of their local bank and set up an IRA as easily as opening a checking account. However, when it comes to estate planning using 401k vs an IRA, there are several important factors that should be considered.

These plans can seem irresistible since they require almost no effort: contributions are automatically deducted and, once set up, no thought needs to go into how much to invest or which funds to choose since the return is based simply on a bank’s declared interest rate. That can all change, however, if your IRA is mutual fund based, in which case investment choices matter. For the recent college grad, or anyone just starting out in their career, IRAs and 401(k) plans are smart options; depending on your age, you may have 20, 30, or even 40 years of contributions ahead of you to build a bountiful retirement account. If only it were that simple.

As your career progresses, your financial priorities will likely shift as well, from simply saving for some distant life in retirement to building upon your wealth in order to capitalize on a long-term financial plan. Investments in IRAs (individual retirement accounts), as well as 401(k) plans, may become a single component within a more complex portfolio. Your participation in these traditional retirement plans may have been the most convenient investment option 15 or 20 years ago, but as a high-net-worth individual with an eye towards the future, you’re probably thinking about how to leverage these investments given their current capital and financial landscape.

Ultimately, what is often most important is not how much these accounts earn along the way, but how much of it you get to keep or pass on to your heirs…

Such a comparison of the pros and cons of IRAs and 401(k) plans is useful in understanding the limitations and risks associated with both, as well as determining which may offer the greatest benefits to individual investors—and how they can effectively complement each other. Ultimately, what is often most important is not how much these accounts earn along the way, but how much of it you get to keep or pass on to your heirs as your estate and legacy planning goals are realized. Together, let’s explore the broader implications for estate planning when investing in a 401(k) vs an IRA—and how to leverage each in order to increase your overall financial portfolio.

Why Estate Planning Is Crucial for High-Net-Wage Individuals

There is a key difference between retirement planning and estate planning. When you plan for retirement, you’re building a nest egg to be used for expenses after you are no longer receive a regular salary. Estate planning, on the other hand, is about passing on your wealth to your family and the charities most important to you. Careless estate planning, or a lack of it, can actually undermine years of excellent investment planning.

Another key element of estate planning is minimizing the estate taxes that your beneficiaries will pay out on the assets that you’ve spent a lifetime building. IRAs and 401(k) plans are considered tax-advantaged retirement savings plans; both are effective wealth-building vehicles for retirement saving and estate planning. Consistent contributions over a lengthy career can result in significant savings that can be passed on to your estate, as well as used for income to live off of in your golden years.

There are some outstanding IRA and 401(k) maximization strategies that allow a retiree to take taxable IRA and 401(k) distributions, net out the tax due and, using the leverage of life insurance, create millions tax free for family and charity.

Individuals who are among the top salaried earners can leverage traditional retirement savings plans to strengthen their overall savings portfolio. Maxing out contributions to both an IRA and a 401(k) over a 30-year career can amount to more than $1 million in assets if the investments yield solid returns. It’s important not to overlook the value of these plans within the broader scope of estate planning, even if the contributions seem trivial year-to-year. Consistent contributions over the course of your career will add significant wealth to your estate.

The Limitations of Estate Planning Using 401K vs. IRAs

If you have invested in a 401(k) or a traditional IRA, your contributions are pre-tax, which has the effect of lowering your current tax liability while you contribute. While you aren’t paying taxes on these contributions now, you will be required to pay them when you withdraw your funds to be used in retirement. That little nuance can really complicate the matter in the future.

A Roth IRA, on the other hand, offers a strong advantage as contributions are taxed as they accrue, which allows for a tax-free disbursement of funds in the future. When considering a retirement savings plan as a component of estate planning, the Roth IRA offers the benefit of allowing you to pass your assets within these funds to your heirs tax-free. However, a Roth IRA does not offer the tax deductibility of a traditional IRA or 401(k) and may not be ideal for everyone depending on age and income.

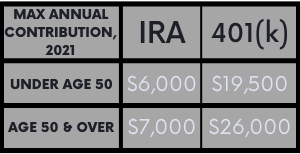

401(k) plans certainly have the advantage over IRAs when comparing contribution limits.

401(k) plans certainly have the advantage over IRAs when comparing contribution limits. Employees can invest up to $26,00 a year and employers are able to match 401(k) plan contributions, increasing the potential principal on which to build your savings. IRAs, on the other hand, are much more restrictive, limiting yearly contributions to no more than $7,000.

Tax Considerations for the 401(k) Plan vs IRAs

If you have invested in a 401(k) or a traditional IRA, your contributions are pre-tax, which has the effect of lowering your current tax liability. While you aren’t paying taxes on these contributions now, you will be required to pay them when you withdraw your funds to be used in retirement.

A Roth IRA, on the other hand, offers a strong advantage as contributions are taxed as they accrue, which allows for a tax-free disbursement of funds in the future. When considering a retirement savings plan as a component of estate planning, the Roth IRA offers the benefit of allowing you to pass your assets within these funds to your heirs tax-free.

Why Estate Planning using 401K and IRAs Can Be Risky Investments

When it comes to risk mitigation, neither the 401(k) nor the IRA offers an advantage over the other. Funds invested in either retirement savings plan generally land in mutual funds, which in turn invest in stock and bonds. These plans are naturally and unavoidably subject to some risks, particularly market volatility.

Investors of mutual funds, stocks, and bonds are well aware that the global stock markets are in a constant state of fluctuation. The greatest fear for many investors is that a stock market slide or crash will result in a loss of not only the financial gains accumulated via a retirement savings plan, but also the principal invested.

Retirement plan advisors remind investors that 401(k) and IRA plans are intended for long-term growth. Your retirement account could see major changes in its value year-over-year, with some years resulting in significant growth and others ending in a loss. There are no certainties with traditional plans. Even if you choose the most conservative strategy, 401(k)s and IRAs offer no guaranteed rate of return.

Before investing in an IRA or 401(k), consider your risk tolerance and invest accordingly, with your estate planning strategy in the forefront of your mind.

Before investing in an IRA or 401(k), consider your risk tolerance and invest accordingly, with your estate planning strategy in the forefront of your mind. Most retirement plans allow you to select which investment vehicles are used for your funds, ranging from no or low-risk options to funds with high-risk portfolios. Younger investors are often advised to invest more aggressively and then move toward conservative funds as they near retirement age. While the rate of return on lower risk investments may not be as great compared to higher-risk opportunities, your peace of mind—and the health of your overall estate—may be well worth the trade-off.

How to Leverage 401(k) and IRA Retirement Plans While Estate Planning

For the purposes of estate planning, the greatest benefits of both 401(k)s and IRAs are realized when you maximize your tax-advantaged savings. This requires maxing out contribution limits. Not every investor has a 401(k) plan available to them but, if you do, contribute as much as you are able in order to reap the full potential of any offered employer matching opportunities. And make it a goal to hit your IRA threshold each and every year.

Remember, the goal of estate planning is to pass on your wealth. Despite the limitations and potential risks outlined above, 401(k) and IRA plans can create a significant financial reserve that not only successfully funds your retirement but also adds impressive value to your estate. A life-long savings strategy results in strong money management habits and years of wealth accumulation. However, as each investor has their own goals for retirement as well as estate planning, it is crucial for investors to consider the advantages and disadvantages of each account, along investment alternatives, with the help of a trusted financial advisor.

The last thing you want to do is leave your heirs a huge, taxable IRA or 401(k) balance that will be reduced to ashes once the IRS is done taxing it.

This is especially true if you combine the power of tax deferred savings over time with effective IRA and 401(k) maximization strategies using life insurance. The problem with estate planning using 401K is that you could be leaving your heirs with a huge, taxable IRA or 401(k) balance that will be reduced to ashes once the IRS is done taxing it. If you reasonably believe your IRA or 401(k) balance will outlive you, then you really need to implement a tax-free maximization strategy.

A life-long savings strategy results in strong money management habits and years of wealth accumulation. However, as each investor has their own goals for retirement, as well as estate planning, it is crucial for investors to consider the advantages and disadvantages of each account, along with investment alternatives, and, ultimately, maximization strategies with the help of a trusted financial advisor.

The team of advisors at Howard Kaye Insurance has created an alternative to the traditional retirement plan: the 401 Kaye. This plan removes the market uncertainties that come with money invested in volatile stocks, bonds, and mutual funds. By rerouting funds that would have otherwise been invested in an IRA or 401(k) into a life insurance policy, you can create a guaranteed, tax-free inheritance which can be used to fund your retirement while adding significant value to your estate.

Contact us to discuss how our team can help you get the most out of your retirement savings for the health of your financial future—and your family’s. Call 1-800-DIE-RICH to be connected to a Howard Kaye advisor today.

Image courtesy Pixabay user EmailMe3