The word audit usually brings to mind the IRS, filing cabinets full of receipts, and the fear that a missed digit on a tax return could cost thousands of dollars in penalties. While one survey found that more than one in 10 Americans fear getting audited, not all audits are created equal. A detailed life insurance policy review is recommended by financial advisors as a positive step toward securing your financial future.

Life insurance is an essential planning tool to ensure that your family is financially secure in the event that you are no longer able to provide for them. Scheduling time once a year for a policy audit and review allows you to make incremental, but impactful, changes to your current policies. Slight adjustments every year, as opposed to trying to overhaul your coverage once a decade, will leave you less vulnerable in an unexpected or untimely life event.

Life insurance is an essential planning tool to ensure that your family is financially secure in the event that you are no longer able to provide for them. Scheduling time once a year for a policy audit and review allows you to make incremental, but impactful, changes to your current policies. Slight adjustments every year, as opposed to trying to overhaul your coverage once a decade, will leave you less vulnerable in an unexpected or untimely life event.

A life insurance policy review is your golden opportunity to assess your existing plan in order to identify any gaps in coverage resulting from a change in your circumstances, your health, or the financial needs of your beneficiaries. It also gives you the chance to dust off old policies and confirm that your beneficiaries are up-to-date, that the policy is performing as intended, and that the coverages will be in effect when you need them. The checklist below outlines the steps for a life insurance policy review—and reinforces the many financial (and peace of mind) benefits to be gained by connecting with a financial advisor for a yearly audit.

The Annual Life Insurance Policy Review Checklist: 7 Easy Steps

A thorough life insurance policy review should start with this checklist. By checking off each box, you’ll be able to assess whether or not you have enough, or the right, coverage—or whether you need to turn to a trusted financial advisor to fill any gaps or update information.

- Step #1: Assess your current policies to determine if you have sufficient insurance coverage.

- Step #2: Review your policies to ensure that coverage has not lapsed and will last as expected.

- Step #3: Update policy beneficiaries if necessary and check that policy ownership is optimal.

- Step #4: Research the financial health of your current insurer.

- Step #5: Evaluate the previous year’s life insurance goals and whether they need to be adjusted.

- Step #6: Protect your estate from taxes by researching potential federal and state tax implications.

- Step #7: Request recommendations for updating your policies from a trusted financial advisor.

Step #1: Assess the Current Coverage of Your Life Insurance Policies

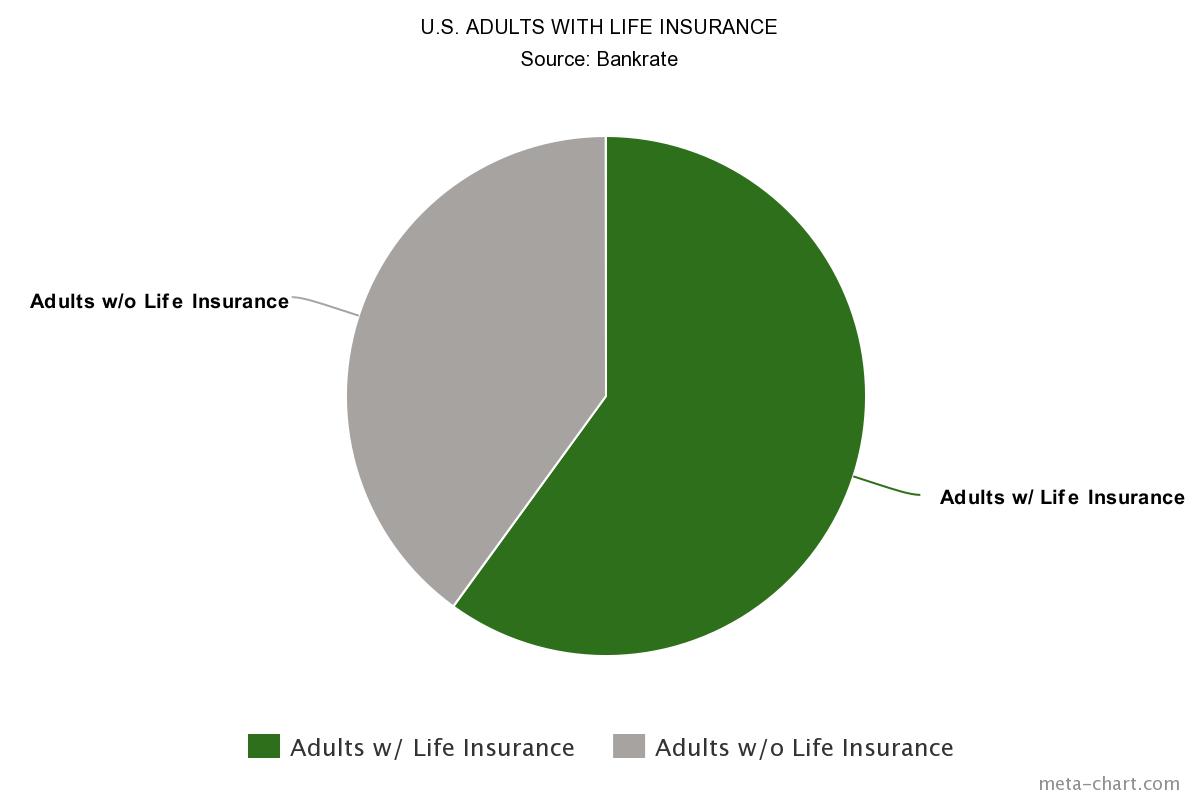

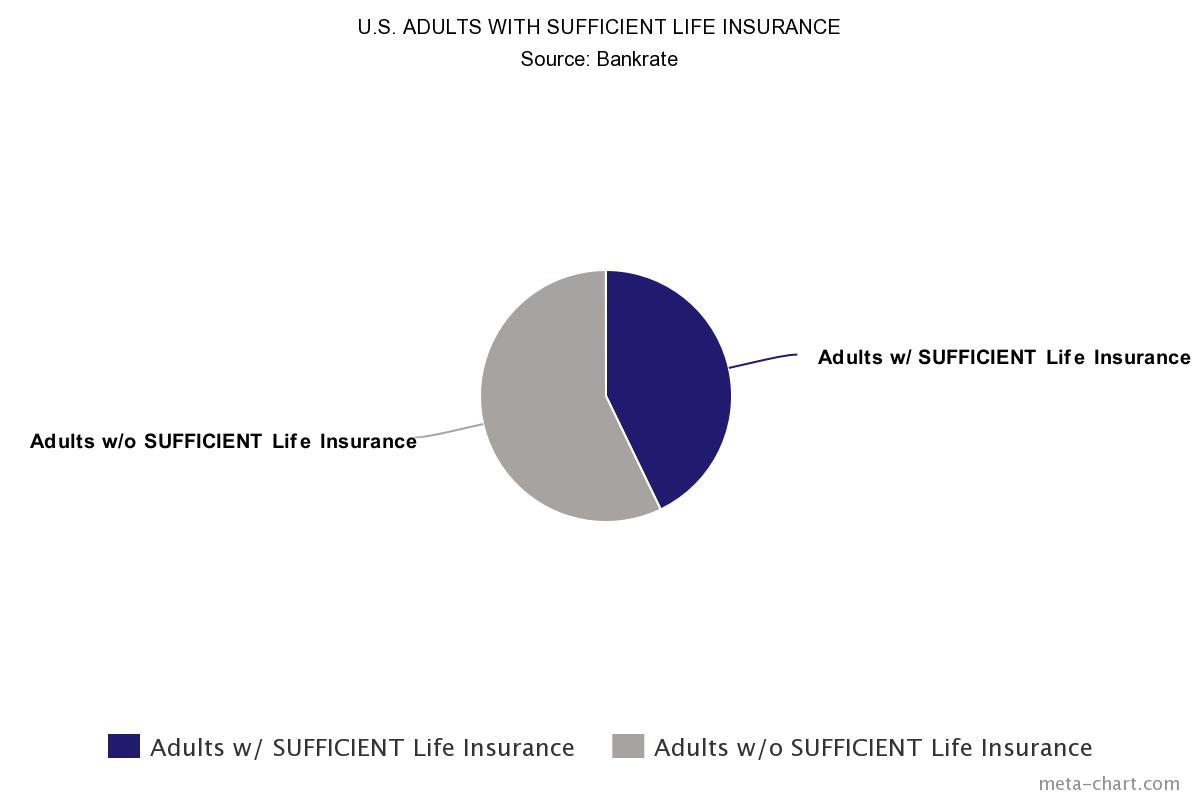

According to research from Bankrate, 60% of Americans have life insurance, but only about half of them have sufficient coverage to protect the actual financial needs of their family. A key goal of any life insurance policy review, therefore, is to determine if your coverage is realistically sufficient should a major life event occur.

According to research from Bankrate, 60% of Americans have life insurance, but only about half of them have sufficient coverage to protect the actual financial needs of their family. A key goal of any life insurance policy review, therefore, is to determine if your coverage is realistically sufficient should a major life event occur.

Life insurance is typically purchased during key life stages, i.e. when you get married or have your first child, and then put on autopilot, as you pay your premiums without much thought. However, as you age or your family grows and spreads its wings, you need to reassess your coverage.

If you have several teens, are you financially prepared for college? Or, alternatively, do married adult children need less protection than when they were children? Also easy to overlook is the rising cost of funeral expenses—something that may not have even been a consideration when you first purchased your policy in your younger years.

Step #2: Review Your Life Insurance Coverage

Life insurance policies that were purchased over 10 years ago may either be out of date or have lapsed—and you may not even be aware of it. For instance, recent retirees often see their generous work-sponsored policy lapse after they step away from their careers.

Life insurance policies that were purchased over 10 years ago may either be out of date or have lapsed—and you may not even be aware of it. For instance, recent retirees often see their generous work-sponsored policy lapse after they step away from their careers.

Workplace life insurance is a common form of coverage but is designed to cover families in the event of the unexpected death of the breadwinner. These policies often end upon separation from a company, including at retirement—a time when excitement for your new life stage can often overshadow insurance policy logistics.

In addition, many universal life policies have seen adjustments to their mortality and expense charges which have had a negative impact on the coverage duration. A policy that was scheduled to last through age 90 may suddenly be on track to lapse at age 83. If that is sooner than your life expectancy, you have a problem that needs to be addressed immediately. A life insurance audit can identify outdated policies so that you can fill any coverage gaps with the help of a financial advisor.

Step #3: Ensure All Your Desired Beneficiaries Are Protected and Ownership Is Correct

Keeping your beneficiaries, as well as your policies, up-to-date is another critical step in your life insurance policy review. Schedules are busy and free time hard to come by, especially after major life events. You may not have made changes to a policy after a divorce or the death of a loved one. Perhaps new grandchildren need to be added as beneficiaries or adult children’s shares reduced.

A life insurance policy review and audit presents an opportunity to confirm the contingent beneficiaries on each of your policies, as well as who will receive the policy proceeds in the event that your primary beneficiary has passed away. The more possibilities that are accounted for when it comes to beneficiaries, the better for the health—and stability—of your family and their financial future.

Ownership is critical as well since improper ownership can lead to very harsh tax treatment. It may be beneficial for policies to be trust-owned or owned by children or someone else depending on circumstances. This is very important and should not be overlooked.

Step #4: Research Your Insurer and Their Services

This step of the life insurance policy review is where it becomes absolutely critical to have the guidance of a professional. The financial health of your insurance company or companies must be assessed on a yearly basis; instability in the financial markets may have had an impact on the company underwriting your policy. A goal of your audit should be to ensure that your provider is still in a good long-term financial position to meet its obligations, including the eventual payout on your policy.

An experienced advisor will have the expertise to review your policies. They can also research your specific life insurance products and if your premiums are in line with your coverage. Insurance costs fluctuate year to year. Your advisor should not only be helping you work toward your long-term goals, but also optimizing your current premiums, potentially saving you money in the short-term as well.

Step #5: Evaluate and Review Your Life Insurance Policy Goals

As you review your life insurance policy coverage, you should evaluate the goals of your current policies. For example, you may have purchased a policy to safeguard your spouse and children, ensuring that the mortgage would be paid and college expenses covered in the event of your untimely death. If your children have graduated and the house has been paid off, however, a policy expert may advise you to reevaluate your goals and make adjustments as necessary. Perhaps your focus can be realigned from covering college expenses to helping your children build up a retirement nest egg, for instance.

Health considerations also fall into this phase of the audit and are a key factor in why experts recommend annual life insurance policy reviews. Your ability to procure a new policy may be tied to your health and expected longevity; an annual assessment will enable you to make coverage adjustments if there has been an unexpected change in either.

Step #6: Protect Your Estate from Taxes

Your financial advisor should have provided guidance on minimizing estate taxes when you initially purchased your policy. However, if your coverage includes employer-sponsored insurance or additional policies you may have purchased separately, they—and you—may not be fully aware of all of the estate tax implications and potential pitfalls. An expert financial advisor will conduct a full review of tax liabilities as part of your life insurance policy audit.

Step #7: Recommendations for Future Life Insurance Policies

After your life insurance policy review checklist has been completed, you should have a clear picture of your current coverage, as well as any potential gaps or oversights. If it turns out that you and your heirs are properly covered, your time investment is still well worth the ROI in terms of greater peace of mind. If, however, there are any gaps in your coverage, your advisor will be in a prime position to recommend the best financial solutions specific to you and your family’s circumstances, which could include additional policies, pre-emptive tax planning, or the inclusion of other financial planning products and services that will help you achieve your goals for a financially secure future.

After your life insurance policy review checklist has been completed, you should have a clear picture of your current coverage, as well as any potential gaps or oversights. If it turns out that you and your heirs are properly covered, your time investment is still well worth the ROI in terms of greater peace of mind. If, however, there are any gaps in your coverage, your advisor will be in a prime position to recommend the best financial solutions specific to you and your family’s circumstances, which could include additional policies, pre-emptive tax planning, or the inclusion of other financial planning products and services that will help you achieve your goals for a financially secure future.

Just as fire departments advise that homeowners use Daylight Savings as a reminder to check the batteries in their smoke detectors once a year, you should consider penciling in a life insurance audit to your yearly calendar as well. The day you choose is of no consequence, so long as you schedule a time, every year, to sit down across from your financial advisor and thoroughly review your existing life insurance policies.

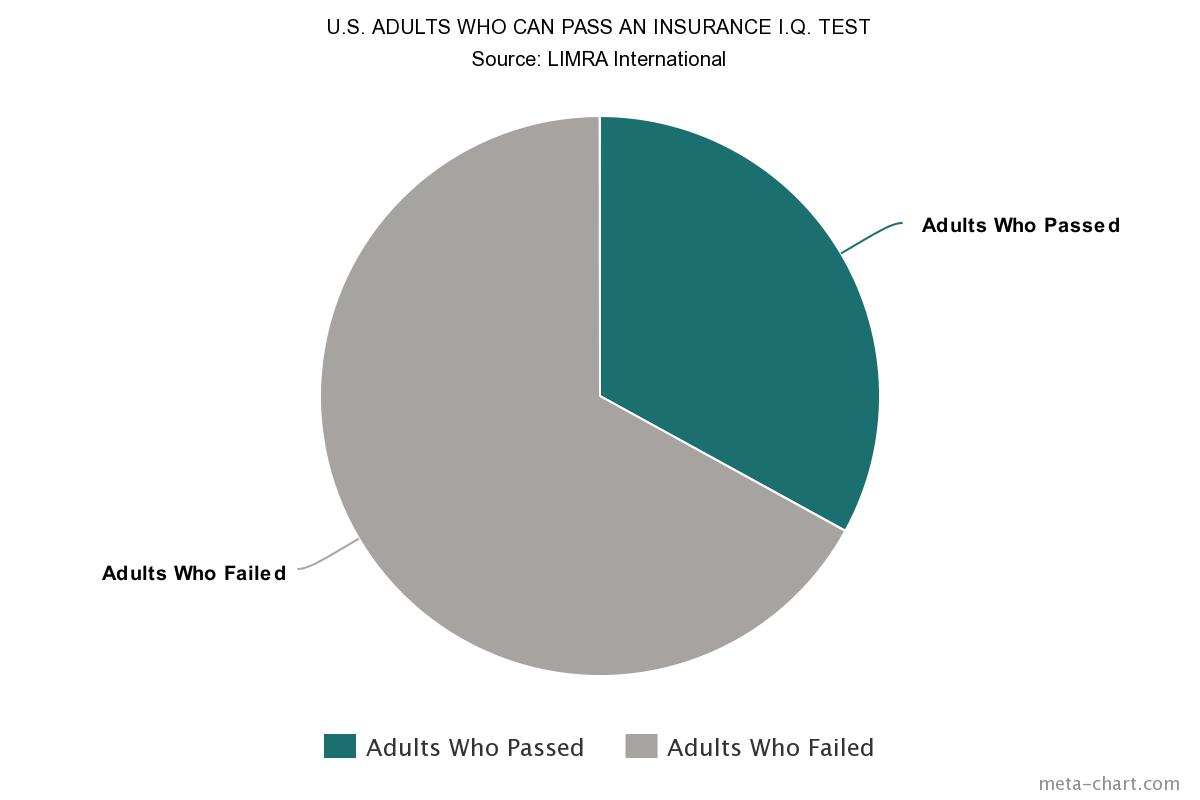

Several years ago, the Life Insurance Market Research Association (LIMRA) conducted a life insurance IQ test; only one-third of consumers passed. Most Americans don’t have a good understanding of life insurance, let alone their specific policies. Take the exam for yourself, then decide if you want to risk the financial health of your heirs when an afternoon sit-down with an advisor could provide all the security you need for the coming year. The risk of insufficient coverage or erroneous policies is significant and could be devastating. Call your advisor today for a life insurance policy audit and review. Don’t leave your financial future to chance.

At Howard Kaye Insurance, my team and I have the expertise to take a holistic approach to estate planning, including assessing life insurance policies and their impacts on your financial security. Our advisors thoroughly review your current policies and do so at no cost to you if we find that you already have proper coverage in place. Contact us today for your free policy review, or call 1-800-DIE-RICH.

Image courtesy Pixabay user StartupStockPhotos