If you’re over the age of 25, you probably have a pretty good recollection of the last recession—and how it eliminated $2.7 trillion from retirement accounts in 2008. I speak to clients every day who are still feeling the impact of those losses nearly 10 years after the recession began despite the current positive stock market news and the Dow hitting record highs on a near monthly basis.

My clients are often looking to consider investment alternatives with greater immunity to market volatility, which caused such extreme losses to traditional retirement options in the not too distant past. Life insurance is often the financial answer that my clients are seeking—when properly structured with the help of an estate planning advisor.

Investors weighing out the benefits of life insurance as an investment alternative generally come to realize that insurance is a very secure choice. The fact is, estates comprised primarily of liquid assets such as stocks, IRAs, 401(k)s, and other traditional retirement accounts can easily and without warning be devastated not only by market volatility but by estate taxes as well.

For that reason, aside from the income tax benefits of life insurance, I would like to explore with you the life insurance investment pros and cons for your retirement and estate—and explain why the most crucial element of your planning will be the advisor you choose.

Life Insurance as an Investment: The Cons for Your Estate

As an insurance advisor, I know first hand that life insurance is often overlooked as one of the most lucrative, yet stable financial vehicles. That being said, for estate planning purposes, there are some cons to using life insurance as a retirement investment alternative:

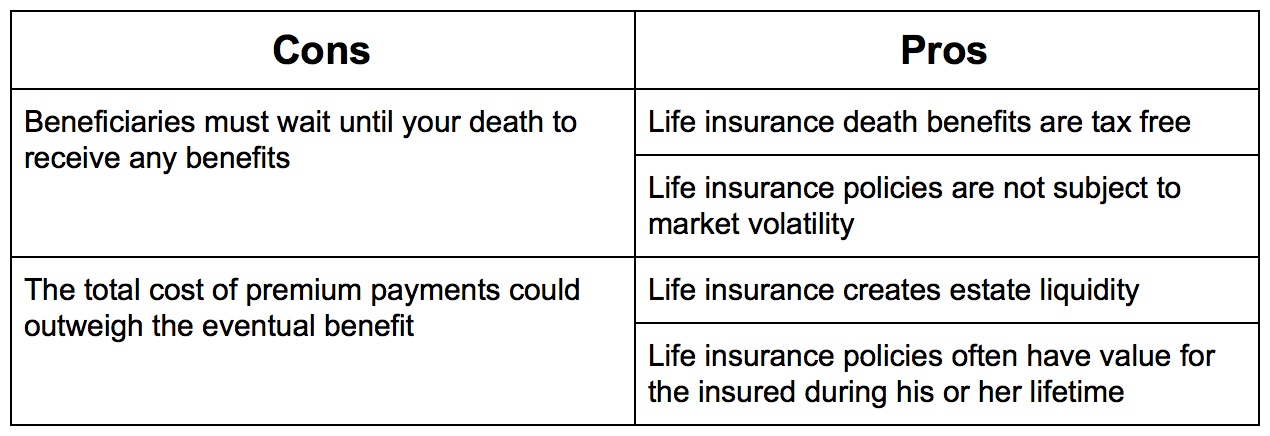

- Con #1: Beneficiaries must wait until your death to receive any benefits. The obvious downside to life insurance is that your beneficiaries cannot receive any funds until your death. This limitation will prevent your heirs, as well as your favored charities, from fully benefiting from the wealth that you intend to share with them until you pass. However, there are options that are complementary to investing in life insurance that will allow you to share your wealth during your lifetime. For instance, annual gifts which can be used to pay for your heirs’ college expenses.

- Con #2: The cost of your premiums could outweigh any benefits in some rare instances. Life insurance policies are structured in such a way that, in aggregate across all policies, insurance companies do not lose money. Underwriters and actuaries have calculated the cost of every policy—in detail. In some rare cases, the premiums that are paid over the lifetime of a policy will exceed the eventual death benefit. For instance, if you live to 100 and your policy requires that you pay premiums until your death, the death benefit will not be as valuable as it would be if you passed away at age 80. Having a trusted life insurance advisor, however, can help you avoid the mistake of overpaying for a policy. They can also work with you to restructure current policies to help you avoid paying out more in premiums than their eventual value.

The Pros of Life Insurance as an Investment Alternative for Your Estate

The pros of life insurance as an investment alternative for estate planning tend to greatly outweigh any cons, with the tax benefits and the stability of its value (outlined below) providing the greatest advantages to your family and heirs.

- Pro #1: Life insurance death benefits are tax-free. Perhaps the most significant benefit to using life insurance as an investment alternative is the fact that the death benefits paid out on life insurance policies are free from income tax—provided they are properly structured with the help of a trusted insurance advisor. Estate taxes and income, on the other hand, can eat up as much as 75% of the total value of your IRAs, 401(k)s, real estate, and stock portfolios.

- Pro #2: Guaranteed life insurance policies are not subject to market volatility. When you purchase a guaranteed life insurance policy, the death benefit is guaranteed. So a $1 million policy will never be valued at less than $1 million when you pass away. Depending on when you pass, the return on your premium investment can be incredibly impressive compared to traditional investments that have risk. The value of your stocks or IRA account, on the other hand, is based on the performance of the underlying investment and can heavily fluctuate. When they perform well, your portfolio may see incredible gains that your heirs can benefit from. However, if the market drops again as it did in 2008, your family may be left with less than you initially invested. In addition, keep in mind that most investments are not tax free!

- Pro #3: Life insurance creates estate liquidity. A key goal of estate planning is to pass on as much of your wealth as possible; interestingly, though, lowering the value of your estate reduces the amount subject to estate taxes. By using liquid assets during your lifetime such as IRA required minimum distributions or annuity payments to pay the premiums on a life insurance policy, you achieve two objectives: you reduce the size of your estate subject to taxes and purchase a life insurance policy that passes wealth on to your beneficiaries free of income taxes. A qualified advisor that specializes in life insurance can help you devise an estate plan that meets both of these goals.

- Pro #4: Life insurance often has value during the insured’s lifetime. There are, of course, ways to share your wealth with family and charities during your lifetime. Often overlooked with life insurance is the option of accessing the cash value which can be based on market indices or dividend and interest growth. In addition, as an alternative to cash surrender, a life settlement may be available, which secures either a cash amount exceeding the surrender value or possibly a paid up death benefit in exchange for selling the policy to an institutional investor. Cashing in a life insurance policy, or securing a life settlement is a weighty decision, but could provide a cash infusion that can be used for covering unexpected health care or nursing home costs, or simply provide greater liquid assets that can be gifted to charities or family members. In summary, with life insurance policies with a cash-out option, surrendering a policy for cash can be a straightforward process, but, with the help of an insurance expert, there could be even greater value in selling a policy through secondary markets. An increased appetite for life insurance policies among institutional investors has created a premium on many policies. Your policy could be worth more than the insurance company’s cash surrender offer.

There are many factors that go into selecting the financial vehicles investments that are right for you. Considering the pros and cons of life insurance shows that there are many advantages to considering it as an investment alternative. However, it is crucial to get the advice of a trusted—and well-qualified—insurance advisor that has the experience to guide you through the decision making process. Your advisor can help you to create a properly structured wealth creation and transfer plan that includes life insurance.

At Howard Kaye Insurance, our team has successfully created and preserved more than $1 billion of wealth, with life insurance playing a key role in our estate planning strategies. Call us today at 800-DIE-RICH or reach out online to discuss how you can leverage life insurance in your estate plan.

Image 1: Image courtesy marchmeena. Image 2: Image courtesy monkeybusinessimages